Key Takeaway

The tightening of leverage by prime brokers signals a structural shift from 'AI euphoria' to 'valuation reality,' threatening a liquidity-driven correction in high-beta Indian tech and EMS stocks.

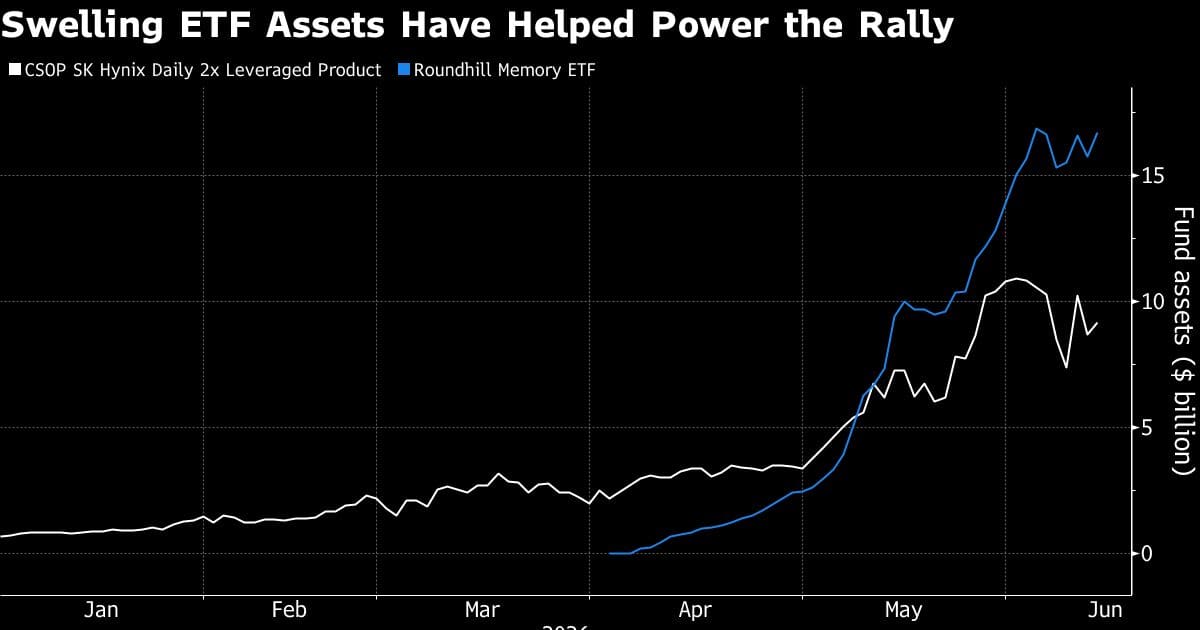

Global financial institutions are hitting the brakes on the semiconductor rally by restricting hedge fund margin lending for South Korean giants Samsung and SK Hynix. This move, driven by fears of an overheating AI sector, is set to trigger a ripple effect across global tech indices. For Indian investors, this signals a period of heightened volatility for high-valuation IT and electronics manufacturing stocks.

The Great De-leveraging: Why Prime Brokers Are Turning Cold on the AI Rally

In the high-stakes world of global finance, prime brokerages—the lending arms of investment banks like Goldman Sachs, Morgan Stanley, and JPMorgan—act as the ultimate arbiters of market liquidity. When these titans decide to tighten the screws on leverage, the tremors are felt from Seoul to Mumbai. Recently, a quiet but significant shift has occurred: global banks have begun restricting the amount of leverage hedge funds can use to bet on Samsung Electronics (KRX: 005930) and SK Hynix (KRX: 000660).

This isn't merely a technical adjustment; it is a profound signal of caution. After a breathtaking rally fueled by the insatiable demand for High Bandwidth Memory (HBM) chips—essential for NVIDIA’s AI processors—valuations have reached levels that make risk managers lose sleep. SK Hynix, for instance, saw its stock price surge over 90% in a year before the recent cooling. By raising margin requirements, banks are effectively saying that the 'Value at Risk' (VaR) has exceeded acceptable thresholds. When leverage is withdrawn, hedge funds are often forced into 'involuntary liquidations,' selling off winners to cover margin calls, which can lead to a cascading sell-off across the global semiconductor ecosystem.

Why does the Samsung and SK Hynix leverage squeeze matter now?

The timing is critical. We are currently in a transition phase where the market is moving from 'hype-based' investing to 'earnings-validated' investing. Samsung and SK Hynix are the bellwethers of the global hardware cycle. If prime brokers fear a bubble in these giants, it implies a broader skepticism toward the entire AI value chain. For the Indian market, which has seen a massive influx of Foreign Institutional Investor (FII) capital into the Electronics Manufacturing Services (EMS) and IT services sectors, this is a clarion call. Historically, when the Philadelphia Semiconductor Index (SOX) or the KOSPI tech heavyweights face a liquidity squeeze, the Nifty IT index follows with a lag of 2-3 weeks, often with amplified volatility.

Deep Market Impact: Connecting the Korean Squeeze to Dalal Street

The correlation between global semiconductor health and Indian equities has strengthened significantly over the last 36 months. This is due to India’s dual role as a consumer of chips (IT Services) and an emerging assembler of electronics (EMS). When liquidity dries up in the primary chip-making hubs, it creates a 'risk-off' sentiment that disproportionately affects high-beta emerging market stocks.

The FII Sentiment Shift

FIIs often view the tech sector as a single global basket. A forced liquidation in South Korean tech often leads to 'sympathy selling' in Indian IT. In 2022, when global tech valuations were reset due to rising yields, the Nifty IT Index corrected by nearly 26%, even as the broader Nifty 50 remained relatively resilient. Currently, with many Indian EMS stocks trading at Price-to-Earnings (P/E) multiples exceeding 100x, the margin for error is non-existent. A reduction in global liquidity means the 'dumb money'—highly leveraged speculative capital—is the first to exit, often triggering stop-losses for institutional players.

How will a global chip correction affect Indian IT and EMS stocks?

The impact is two-fold: valuation derating and supply chain uncertainty. Indian IT firms like Tata Elxsi and L&T Technology Services (LTTS) depend on R&D spending from global semiconductor and automotive giants. If Samsung or SK Hynix signal a slowdown or face a stock price collapse, their CAPEX and R&D budgets eventually tighten. Furthermore, companies like Dixon Technologies and Kaynes Technology, which are the darlings of the 'Make in India' initiative, rely on the steady pricing and availability of components. A volatile semiconductor market leads to inventory hoarding or price spikes, both of which are margin-dilutive for Indian assemblers.

Stock-by-Stock Breakdown: The Indian Casualties

As the global de-leveraging play unfolds, several NSE-listed stocks are in the direct line of fire. Here is an analysis of the most vulnerable players:

1. Dixon Technologies (NSE: DIXON)

Context: Dixon is the poster child for India’s EMS boom, with a market cap exceeding ₹70,000 crore. However, it trades at a staggering trailing P/E of approximately 160x.

The Impact: Dixon’s business model relies on high-volume, low-margin assembly. Any volatility in the global semiconductor supply chain—often a byproduct of financial instability at the chip-maker level—impacts their working capital cycle. If FIIs begin a sector-wide rotation out of 'expensive tech,' Dixon is usually the first port of call for profit booking.

2. Tata Elxsi (NSE: TATAELXSI)

Context: Focused on Engineering, Research, and Development (ER&D), Tata Elxsi is deeply embedded in the semiconductor and automotive electronics ecosystem.

The Impact: With a P/E ratio hovering around 65x, the stock is priced for perfection. The company’s growth is tied to the next generation of AI and EV chips. A liquidity-driven sell-off in Samsung/SK Hynix signals a cooling of the very 'AI-fever' that sustains Tata Elxsi’s premium valuation. Watch for a test of the ₹6,800 support level if global sentiment sours.

3. Kaynes Technology (NSE: KAYNES)

Context: A leading player in integrated electronics manufacturing, Kaynes has been a multibagger since its IPO.

The Impact: Kaynes is more sensitive to 'component liquidity.' If global banks are restricting leverage on chipmakers, it often precedes a period of tightening credit for the entire supply chain. Kaynes’ aggressive expansion plans into OSAT (Outsourced Semiconductor Assembly and Test) facilities make it highly sensitive to global semiconductor sentiment.

4. L&T Technology Services (NSE: LTTS)

Context: A pure-play ER&D service provider with significant exposure to the 'high-tech' vertical.

The Impact: LTTS recently signaled a cautious outlook on certain segments of the tech spend. A global pullback in semiconductor stocks would likely lead to a further 'valuation haircut' for LTTS, which has struggled to maintain its historical growth premiums compared to mid-cap IT peers like Persistent Systems.

5. CG Power & Industrial Solutions (NSE: CGPOWER)

Context: Entering the semiconductor ATMP (Assembly, Testing, Marking, and Packaging) space in a joint venture.

The Impact: The stock’s recent re-rating was largely based on its semiconductor ambitions. If the global 'AI and Chip' narrative shifts from 'unbridled growth' to 'leverage-restricted caution,' the speculative premium in CG Power’s stock price could evaporate quickly.

Expert Perspective: The Bull vs. Bear Case

"We are seeing a classic 'Prime Brokerage Squeeze.' It’s not that the fundamentals of AI have changed overnight, but the cost of carrying a levered position has become prohibitive. This will lead to a healthy, albeit painful, flush-out of weak hands." — Senior Portfolio Manager, WelthWest Research

The Bear View: Bears argue that the AI rally was built on a foundation of cheap debt and excessive leverage. With banks now restricting margin, the 'virtuous cycle' of rising prices leading to more borrowing is broken. They point to the 2000 Dotcom crash, where the hardware makers (Cisco, Intel) crashed first, followed by the service providers. They expect a 15-20% correction in Indian EMS stocks as valuations mean-revert.

The Bull View: Bulls suggest this is a temporary 'speed bump.' They argue that the demand for HBM chips by NVIDIA is real and backed by cash flows, unlike the 2000 bubble. They see any dip in Indian stocks like Dixon or Kaynes as a 'generational buying opportunity,' citing the structural shift of manufacturing from China to India (China+1 strategy).

Actionable Investor Playbook: Navigating the Volatility

How should a retail or HNI investor react to this global de-leveraging event?

- Tactical Sell: Reduce exposure to stocks with P/E ratios 2 standard deviations above their 5-year mean. Specifically, look at EMS players trading above 100x P/E.

- Defensive Rotation: Shift capital toward 'Value' IT. Large-cap players like Infosys (NSE: INFY) or HCL Tech (NSE: HCLTECH) have already undergone significant valuation time-corrections and offer better dividend yields and safety margins.

- Watch the KOSPI: Monitor the 20-day moving average of SK Hynix. If it breaks decisively below, expect a secondary wave of selling in Indian high-beta tech.

- Entry Points: For long-term believers in the Indian semiconductor story, wait for a 15% correction from recent highs in Kaynes or Dixon before initiating new positions. The goal is to buy when the 'leverage' has been fully purged from the system.

Risk Matrix: What Could Go Wrong?

| Risk Factor | Probability | Impact Assessment |

|---|---|---|

| Forced Margin Liquidations | High | Could trigger a 5-7% flash crash in global tech indices. |

| FII Outflow from India | Medium | High-valuation EMS stocks could see a 15% drawdown. |

| AI Earnings Miss | Low | Would validate the 'bubble' thesis and lead to a structural bear market in tech. |

What to watch next?

Investors should keep a close eye on the following catalysts over the next 30 days:

- NVIDIA’s Next Earnings Call: Any guidance cut or mention of supply chain 'normalization' will accelerate the sell-off.

- US Federal Reserve Minutes: If the Fed remains hawkish, the 'cost of carry' for leveraged trades will stay high, prolonging the de-leveraging phase.

- South Korean Export Data: Released monthly, this is the most accurate real-time indicator of global chip demand.

- Institutional Delivery Volumes on NSE: Watch if the selling in Dixon or Tata Elxsi is accompanied by high delivery volumes, indicating institutional exit rather than just retail panic.

Disclaimer: This content is generated by WelthWest Research Desk based on publicly available reports and is for informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Always consult a qualified financial advisor before making investment decisions.