Key Takeaway

The convergence of a sustained AI-led productivity cycle and a fragile Yen carry trade creates a high-conviction environment for Indian IT exporters, provided investors navigate the looming risk of a Bank of Japan liquidity pivot.

The global market is currently defined by an AI-fueled tech resurgence and the historic weakening of the Japanese Yen. This dual-force dynamic is creating a unique tailwind for Indian IT services, though the threat of a sudden BoJ intervention looms over global liquidity flows. This deep dive examines the risks and opportunities for investors in the Nifty IT sector.

The Great Liquidity Shift: AI, the Yen, and Indian Equities

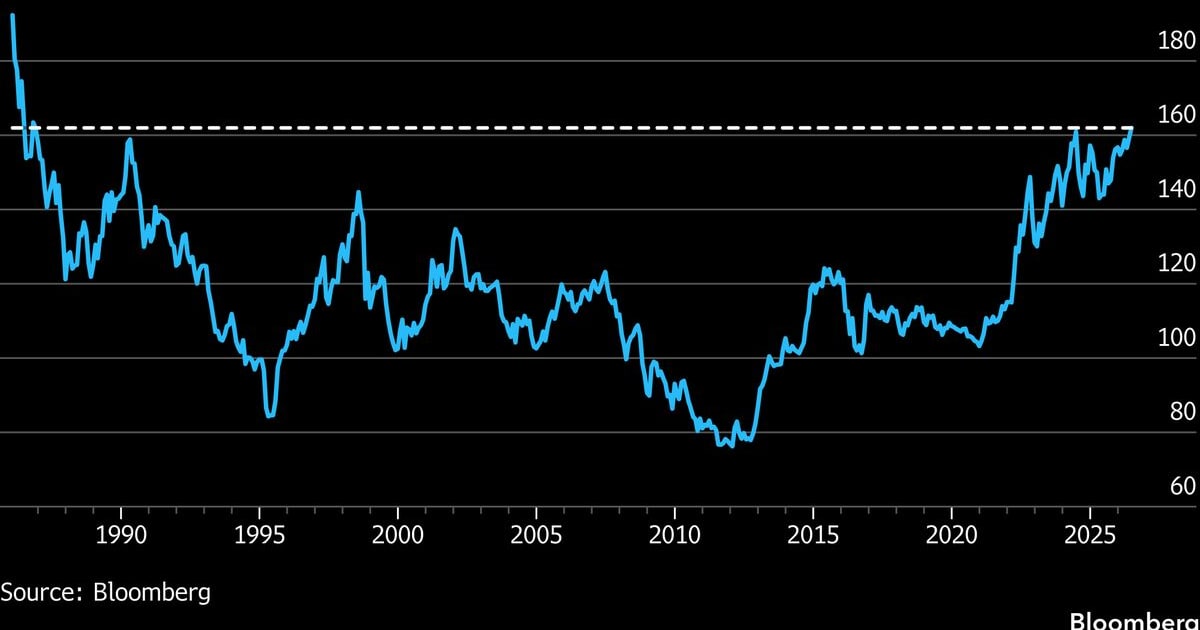

Global capital markets are currently navigating a fascinating dichotomy: a relentless, AI-driven valuation expansion in the technology sector and a historic collapse in the Japanese Yen. For the astute investor, this is not merely a currency story—it is a structural reconfiguration of global liquidity flows. As the Yen hits multi-decade lows, the 'carry trade'—borrowing in low-interest Yen to invest in higher-yielding assets—has become the lifeblood of current market buoyancy.

For the Indian investor, this dynamic is critical. As global tech capital pivots toward high-growth AI infrastructure, Indian IT services are being re-rated from 'cost-optimization' plays to 'digital transformation' essentialists. However, the fragility of the Yen suggests that this liquidity party may have a firm expiration date.

Why does the Yen’s weakness matter to the Indian IT sector?

The Yen serves as the world’s primary funding currency. When the Yen is weak, Japanese investors seek yield elsewhere, often flooding into emerging markets like India. Historically, when the Yen depreciates rapidly, we observe a positive correlation with Nifty IT performance, as global tech budgets remain tethered to the aggressive capital expenditure cycles of the US 'Magnificent Seven.' In 2022, when the Yen first began its sharp slide, we saw a temporary disconnect; today, the correlation is tighter, as AI demand provides a structural floor for Indian export earnings.

How will a Bank of Japan (BoJ) policy shift impact Indian IT exporters?

The primary risk is a 'liquidity crunch.' If the BoJ intervenes to defend the Yen, the carry trade will unwind violently. This would necessitate a massive repatriation of capital, likely leading to a broad-based selloff in emerging market equities. For Indian IT firms, this would manifest as a sudden tightening of US client budgets as global liquidity vanishes, potentially impacting the high P/E multiples currently enjoyed by the sector.

Stock-by-Stock Analysis: Navigating the Nifty IT Landscape

- TCS (TATA CONSULTANCY SERVICES): As the industry bellwether, TCS currently trades at a P/E of ~30x. Its massive scale makes it the primary beneficiary of enterprise-wide AI implementation. The weak Yen indirectly supports TCS by keeping the broader risk-on sentiment alive for its Fortune 500 clients.

- INFY (INFOSYS): Infosys is aggressively pivoting toward Generative AI. With a strong pipeline in cloud and data modernization, it remains a core holding for institutional investors seeking to hedge against domestic volatility through US dollar-denominated revenue.

- HCLTECH: HCL’s focus on engineering and R&D services positions it perfectly to capture the 'AI hardware and software integration' spend. It remains more sensitive to global cyclical shifts than TCS, making it a higher-beta play.

- WIPRO: Currently undergoing a strategic turnaround, Wipro represents a 'value' play within the sector. It is less exposed to the immediate AI-hype valuation bubble but stands to benefit from any rotation into laggards if the tech rally broadens.

- TECHM (TECH MAHINDRA): Tech Mahindra’s reliance on the telecom vertical makes it the most sensitive to 5G-AI infrastructure spend. It is a high-risk, high-reward proxy for global network modernization.

Expert Perspective: The Bull vs. Bear Divide

The Bull Case: AI is not a bubble; it is a fundamental shift in unit labor productivity. Indian IT services are the 'shovels' in this gold rush. As long as US corporate margins remain resilient, Indian IT will continue to deliver double-digit earnings growth, decoupling from broader liquidity risks.

The Bear Case: Valuations in the Nifty IT space have outpaced reality. The sector is trading at a significant premium to its five-year average. Any 'black swan' event involving the Yen or a US recession would lead to a rapid 15-20% correction as growth expectations are reset.

Actionable Investor Playbook

Investors should adopt a 'barbell' strategy. Maintain core holdings in high-cash-flow giants like TCS and Infosys, which have the balance sheets to survive a liquidity crunch. Simultaneously, hedge exposure by monitoring the USD-JPY cross-rate. If the Yen breaks below critical support levels, consider increasing cash allocations to 20% of your portfolio to capitalize on a potential 'liquidity-crunch' dip.

Risk Matrix

| Risk Factor | Probability | Impact |

|---|---|---|

| BoJ Aggressive Rate Hike | Medium | High |

| US Tech Earnings Miss | High | Medium |

| Geopolitical Currency Intervention | Low | Very High |

What to watch next?

Investors must keep a close watch on the upcoming US Fed meeting minutes and the Bank of Japan’s quarterly policy review. Any signal of a shift in the 'Yield Curve Control' (YCC) framework will be the primary catalyst for a global market repricing. Additionally, monitor the quarterly commentary from US cloud hyperscalers; their capital expenditure guidance is the single most important leading indicator for Indian IT revenue growth over the next 18 months.

Disclaimer: This content is generated by WelthWest Research Desk based on publicly available reports and is for informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Always consult a qualified financial advisor before making investment decisions.