Key Takeaway

The structural floor of the Indian equity market is being tested as FII ownership hits 2016 levels, shifting the entire burden of price discovery onto Domestic Institutional Investors (DIIs) and creating a high-stakes valuation reset for Nifty large-caps.

Foreign Institutional Investors (FIIs) have reduced their Indian equity exposure to levels not seen in a decade, driven by a pivot toward AI-centric markets and concerns over India's persistent valuation premium. This deep-dive explores the mechanics of this capital flight, the vulnerability of the private banking sector, and how retail investors must reposition their portfolios as the 'liquidity safety net' thins. We analyze the specific impact on heavyweights like HDFC Bank and Reliance, providing an actionable roadmap for a high-volatility environment.

The Great Liquidity Reset: Deciphering the Decade-Low FII Footprint

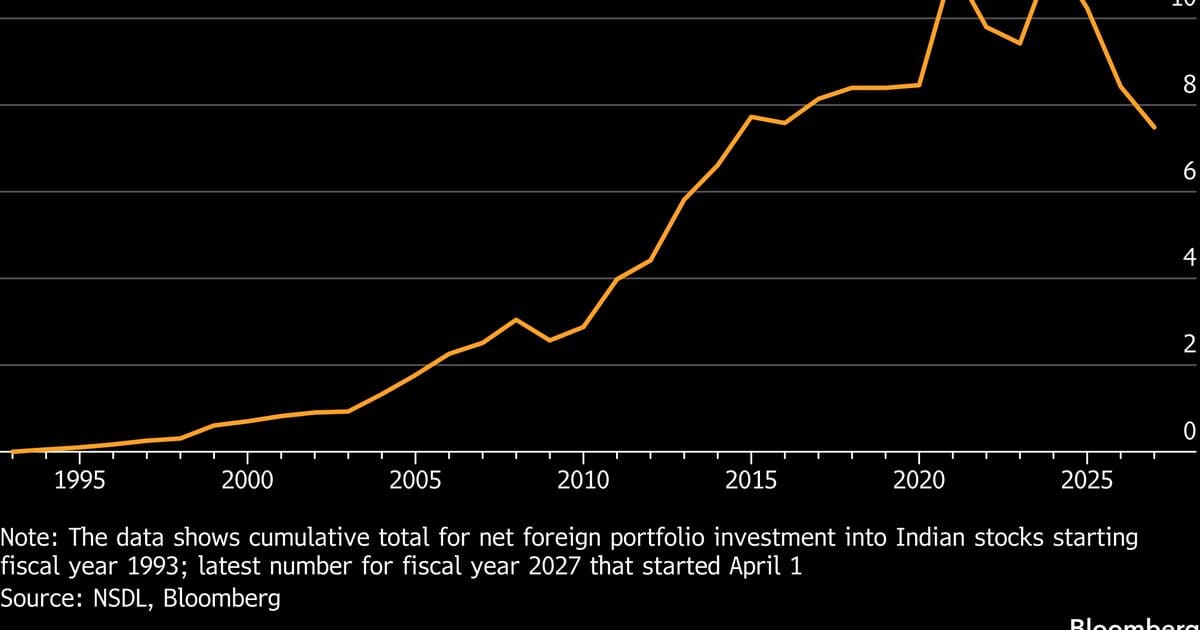

For the better part of a decade, Foreign Institutional Investors (FIIs) were the undisputed kingmakers of the Indian capital markets. Their inflows dictated the direction of the Nifty 50 and the Sensex, providing the deep-pocketed liquidity required to sustain India's premium valuation compared to emerging market peers. However, a tectonic shift is underway. Recent data suggests that FII ownership in Indian equities has plummeted to its lowest level since 2016, effectively erasing nearly ten years of incremental positioning in a relentless multi-month sell-off.

This is not a standard cyclical exit. As of late 2024, the cumulative selling pressure has seen tens of billions of dollars exit the National Stock Exchange (NSE). While Domestic Institutional Investors (DIIs), fueled by robust Systematic Investment Plan (SIP) inflows from retail participants, have acted as a formidable bulwark, the structural integrity of the market is being challenged. When FIIs—who typically manage long-term pension and sovereign wealth funds—exit at this scale, they aren't just selling stocks; they are expressing a lack of confidence in the immediate risk-reward ratio of the Indian macro story relative to global alternatives.

"The Indian market is currently experiencing a 'valuation divorce.' Foreign capital is no longer willing to pay a 50-70% premium over other emerging markets when the U.S. technology sector offers AI-driven growth and China offers deep-value recovery plays."

Why are FIIs selling Indian stocks right now?

The exodus is driven by a 'perfect storm' of three distinct factors: Valuation Fatigue, The AI Magnet, and The China Rebalancing. India’s Nifty 50 has been trading at a 12-month forward P/E (Price-to-Earnings) ratio of approximately 22x to 24x, significantly higher than its historical average of 18x. In contrast, markets like the S&P 500 offer exposure to the generative AI revolution, which is currently perceived as a more immediate 'alpha' generator than India’s long-term demographic dividend.

Furthermore, the 'Basis Trade' has shifted. With U.S. Treasury yields remaining relatively high, the 'carry trade'—where investors borrow in low-interest environments to invest in high-growth markets like India—has lost its luster. When you factor in the Indian Rupee (INR) depreciation against the USD, the net returns for a dollar-based investor in the Indian market have been underwhelming compared to the Nasdaq's performance over the last 18 months.

Deep Market Impact: A Sectoral Breakdown of the Carnage

The impact of FII selling is disproportionately felt because foreign funds are concentrated in the 'Heavyweights.' FIIs traditionally own roughly 30-40% of the free float in India’s largest private banks and IT services firms. When they hit the 'sell' button, they don't sell the broader market; they sell the most liquid names to ensure they can exit without causing a total price collapse.

The Banking Sector: The FII 'ATM'

The private banking sector, specifically the Nifty Bank index, has borne the brunt of this capital flight. For global funds, Indian private banks were the proxy for India's GDP growth. However, as credit growth slows and Net Interest Margins (NIMs) face pressure due to rising cost of funds, FIIs have utilized these highly liquid stocks as 'ATMs' to fund redemptions or reallocate to other markets. This has led to a persistent underperformance of the banking sector despite strong balance sheets.

Historical Parallels: Is 2024 the New 2013?

The last time we saw a structural shift of this magnitude was during the 'Taper Tantrum' of 2013 and the initial rate-hike cycle of 2022. In 2022, FIIs pulled out nearly ₹1.2 lakh crore, leading to a Nifty correction of approximately 15% from its peaks. However, the current sell-off is more insidious because it occurs against a backdrop of record-high domestic participation. This creates a 'false sense of security'—while the index may not crash, the underlying valuation derating (stocks trading at lower P/E multiples) is already happening.

Stock-by-Stock Breakdown: The Casualties of Capital Flight

- HDFC BANK (HDFCBANK): As the stock with the highest FII holding in India, HDFC Bank is the primary target during any mass exit. Post-merger, the bank is struggling with liquidity coverage ratios and stagnant deposit growth. FIIs, who once viewed this as a 'buy and forget' stock, are now trimming positions as the ROE (Return on Equity) normalization takes longer than expected. Sector Peers: Axis Bank, Kotak Mahindra Bank.

- RELIANCE INDUSTRIES (RELIANCE): As the heavy lifter of the Nifty 50, Reliance is often sold by FIIs to reduce overall India exposure. Despite its foray into New Energy and Retail, the stock's massive market cap makes it a liquidity provider for exiting funds. Any sustained FII selling puts an immediate cap on Nifty's upside.

- ICICI BANK (ICICIBANK): While ICICI has outperformed HDFC Bank operationally, it remains vulnerable to FII flows. It is a 'consensus long' for most foreign funds; when a fund manager receives a redemption request, ICICI is often sold simply because it is a profitable position that can be exited quickly.

- INFOSYS (INFY) & TCS (TCS): The IT giants are facing a double whammy. Global macro uncertainty is slowing discretionary spending in the US and Europe, while FIIs are rotating out of traditional IT services into 'Pure Play AI' companies listed on the NYSE/Nasdaq. This has led to a valuation ceiling for Indian IT services.

- KOTAK MAHINDRA BANK (KOTAKBANK): With significant foreign institutional ownership and recent regulatory hurdles regarding its digital banking infrastructure, Kotak has seen a sharp de-rating. FIIs are sensitive to regulatory risks, and any friction with the RBI often triggers an immediate sell-response.

How will RBI rate policy affect FII flows?

A common question among investors is whether a pivot by the Reserve Bank of India (RBI) could reverse this trend. Historically, FIIs return to emerging markets when the interest rate differential between the US Fed and the RBI widens in favor of India, or when the RBI signals a pro-growth stance. However, if the RBI cuts rates too early, it might lead to further INR depreciation, which actually discourages FIIs as their dollar-denominated returns shrink. Investors should watch for the RBI's stance on 'durable liquidity' as a signal for market stabilization.

Expert Perspective: The Bull vs. Bear Case

The Bear Case: Analysts at global firms argue that India is in the midst of a 'Time Correction.' With earnings growth slowing down to the mid-teens and valuations still at a premium, there is no immediate catalyst for FIIs to return. They argue that capital is moving to 'cheaper' alternatives like Southeast Asia or the revitalized Japanese market.

The Bull Case: Contrarian investors suggest that the 'DII absorption' is a sign of India's maturing financial ecosystem. They argue that once the US Fed begins a sustained rate-cutting cycle, the 'Search for Yield' will inevitably bring FIIs back to the fastest-growing major economy. They view the current decade-low holding as a 'capitulation point'—historically, when FII holdings hit such lows, a massive multi-year rally often follows.

Actionable Investor Playbook: Navigating the Exodus

In an environment where the primary price-setters (FIIs) are exiting, retail investors must shift from 'momentum chasing' to 'valuation-conscious' investing.

- Defensive Reallocation: Increase exposure to Consumer Staples (FMCG) and Pharma. These sectors are less dependent on FII flows and provide a hedge against currency volatility. Tickers to watch: HUL, SUNPHARMA.

- The 'Cash is King' Strategy: Maintain 15-20% of the portfolio in liquid funds or short-term debt. This 'dry powder' will be essential if FII selling triggers a final, sharp 'capitulation dip' in large-caps.

- Focus on Domestic Cyclicals: Look for companies that benefit from government CAPEX and domestic consumption, which are less sensitive to global fund flows. Infrastructure and Power sectors remain attractive.

- Entry Points: For long-term investors, the 200-day Moving Average (DMA) on the Nifty 50 should be the primary monitoring level. A breach below this could offer a generational buying opportunity in high-quality private banks.

Risk Matrix: Assessing the Downside

| Risk Factor | Probability | Impact | Mitigation |

|---|---|---|---|

| Persistent Rupee Depreciation | High | High | Hedge with Export-oriented units (IT/Pharma) |

| Global AI Bubble Burst | Medium | Extreme | Stick to value-based Large-caps |

| Domestic SIP Slowdown | Low | Extreme | Monitor AMFI monthly data closely |

| Geopolitical Oil Shock | Medium | High | Increase exposure to Energy/New Energy stocks |

What to Watch Next: The Catalysts for a Reversal

Investors should keep a close eye on three specific triggers that could signal the end of the FII exodus:

- The 10-Year US Treasury Yield: A sustained drop below 3.8% will likely trigger a risk-on sentiment for emerging markets.

- MSCI Rebalancing: Watch for any increase in India's weightage in the MSCI Emerging Markets Index, which forces passive FII inflows.

- Quarterly Earnings Trajectory: If Nifty 50 companies can deliver beat-and-raise quarters despite high interest rates, the valuation argument for FIIs becomes undeniable.

The current landscape is a test of patience. While the exit of foreign capital is creating significant headwinds, it is also clearing the froth from the market. For the disciplined investor, the decade-low FII holding isn't a signal to panic—it's a signal to prepare for the next structural upcycle.

Disclaimer: This content is generated by WelthWest Research Desk based on publicly available reports and is for informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Always consult a qualified financial advisor before making investment decisions.