Key Takeaway

The deepening Russia-China axis and unresolved US-China trade friction act as a dual-catalyst: accelerating the 'China Plus One' shift for Indian manufacturers while introducing energy-led inflation risks that favor domestic self-reliance plays.

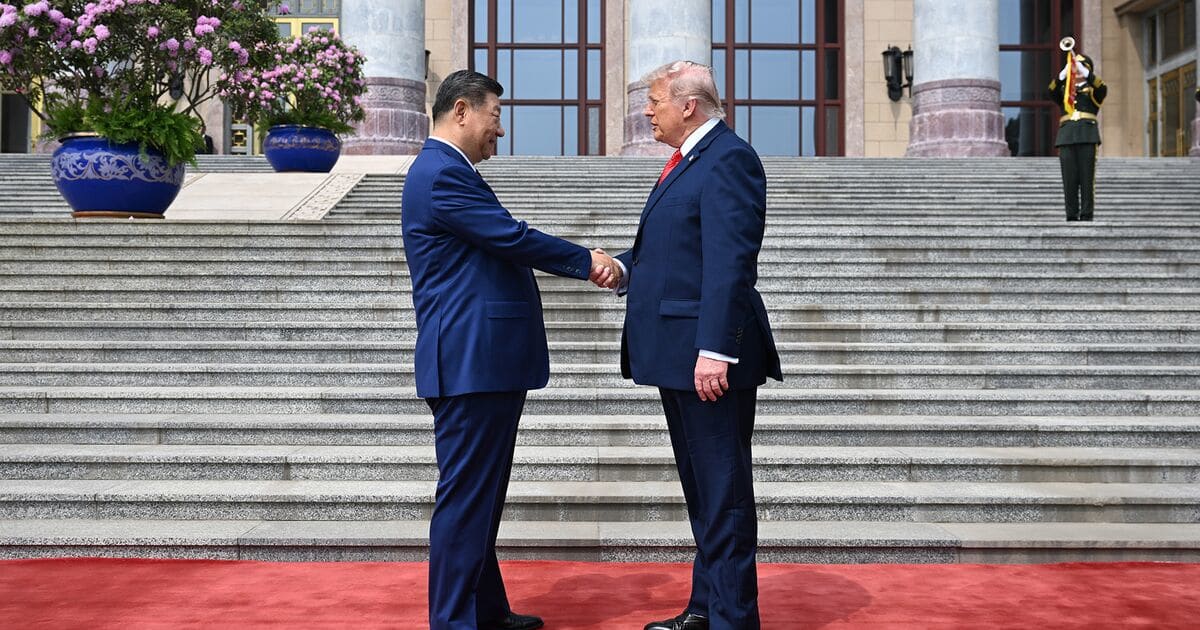

As high-stakes diplomacy unfolds in Beijing with visits from both Donald Trump and Vladimir Putin, the global supply chain is hitting a critical inflection point. While the US seeks trade leverage and Russia seeks a strategic lifeline, India emerges as the structural beneficiary of a fragmented world. This report analyzes the multi-billion dollar shift toward NSE-listed manufacturing giants and the hidden risks of a new geopolitical energy order.

The Beijing Pivot: A Geopolitical Tectonic Shift

The global financial landscape is currently witnessing a rare alignment of geopolitical stars. With Donald Trump and Vladimir Putin making high-profile visits to Beijing, the narrative of 'globalization' is being replaced by 'fragmentation.' For the Indian equity markets, this isn't just a news cycle—it is a fundamental repricing event. The core of this shift lies in the unresolved trade tariffs between Washington and Beijing. Despite the 'historic' optics of Trump’s visit, the underlying friction remains: the US is committed to decoupling, and China is increasingly looking toward a 'Fortress Eurasia' alliance with Russia.

For investors on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE), this creates a 'Goldilocks' scenario for manufacturing but a 'Gordian Knot' for energy. The 'China Plus One' strategy is no longer a boardroom buzzword; it is a survival mandate for global OEMs (Original Equipment Manufacturers). As Trump signals a potential 'Trade War 2.0' and Putin cements a strategic energy-for-technology swap with Xi Jinping, India stands as the only democratic, large-scale alternative with the labor arbitrage and policy support (via PLI schemes) to absorb redirected capital.

How will the US-China trade war affect Indian manufacturing stocks?

The primary beneficiary of the US-China stalemate is the Indian Electronic Manufacturing Services (EMS) sector. Historically, when the US imposed Section 301 tariffs on Chinese electronics in 2018, the Nifty 50 saw a temporary dip, but domestic manufacturing indices began a multi-year re-rating. Today, the stakes are higher. India’s PLI (Production Linked Incentive) schemes have matured, and companies like Dixon Technologies (DIXON) are no longer just assemblers but are moving up the value chain into component manufacturing.

When global tech giants look to de-risk their supply chains away from the 'Dragon,' the 'Tiger' is the natural beneficiary. We are seeing a structural shift in CAPEX. In FY24, India's electronics exports surged to over $29 billion, a testament to this transition. The market is currently pricing in a 25-30% CAGR for top-tier EMS firms over the next three years, driven almost entirely by the vacuum created by US-China decoupling.

The Russia-China Axis: The Energy Wildcard

While the manufacturing narrative is bullish, the strengthening Putin-Xi alliance introduces a 'Risk Premium' to India’s macro-stability. Russia and China are moving toward a 'No Limits' partnership that could see Russian energy diverted almost exclusively to the East. For India, which imports over 80% of its crude oil, this is a double-edged sword. While India has benefited from discounted Russian Urals since 2022—saving an estimated $7 billion in its import bill—a formal Russia-China energy bloc could tighten global supply and lead to volatile Brent prices.

This geopolitical realignment directly impacts Reliance Industries (RELIANCE) and other downstream OMCs. If global logistics are disrupted by new sanctions or 'secondary sanctions' targeting those who deal with the Russia-China bloc, the cost of shipping and insurance will spike, eating into Gross Refining Margins (GRMs). We estimate that every $10 increase in Brent crude adds approximately 50-60 basis points to India’s CPI inflation, potentially delaying the RBI’s pivot to lower interest rates.

Sector-Level Breakdown: Winners and Losers

The Winners: Atmanirbhar Champions

- Contract Manufacturing (EMS): As global brands like Apple and Samsung diversify, Indian firms are capturing the 'China Plus One' overflow. The focus is on scalability and precision.

- Specialty Chemicals: China’s environmental crackdown combined with geopolitical 'de-risking' is pushing global pharma and agrochem majors toward Indian suppliers. This is a high-margin, sticky business.

- Defence: The Russia-China axis forces India to accelerate its domestic defence production. The 'Negative Import List' is the biggest tailwind for this sector in decades.

- Renewable Energy: To mitigate the risk of high oil prices, the Indian government is doubling down on green hydrogen and solar, benefiting domestic module manufacturers.

The Losers: The Vulnerable Links

- Global Logistics & Freight: Increased geopolitical friction leads to 're-shoring,' which reduces long-haul shipping volumes and increases operational costs due to rerouting.

- China-Dependent Tech Hardware: Companies that rely on cheap Chinese sub-components without a local alternative will face margin compression as tariffs rise.

- Oil & Gas Importers: Pure-play importers are at the mercy of the geopolitical 'Fear Premium' in crude markets.

Stock-by-Stock Breakdown: The WelthWest Selection

1. Dixon Technologies (DIXON) | Sector: EMS

Dixon Technologies is the poster child for India's manufacturing prowess. With a market cap exceeding ₹60,000 crore and a P/E ratio that reflects its high-growth trajectory, Dixon is capturing the shift in mobile, lighting, and home appliance manufacturing. As Trump’s rhetoric on China intensifies, Dixon’s partnerships with global OEMs (like Xiaomi and Motorola) become more strategic. Historical Parallel: Since the 2020 border tensions with China, Dixon’s stock has outperformed the Nifty 50 by over 400%, proving that geopolitical friction is its primary fuel.

2. SRF Ltd (SRF) | Sector: Specialty Chemicals

SRF operates in the high-entry-barrier fluorochemicals space. As global supply chains move away from Chinese chemical clusters due to both environmental regulations and geopolitical risk, SRF is perfectly positioned. With a diversified revenue stream and a focus on high-value R&D, SRF acts as a hedge against China. Its current P/E of ~35x is attractive compared to its 5-year average, especially as it ramps up CAPEX in its chemical business.

3. Hindustan Aeronautics (HAL) | Sector: Defence

HAL is the ultimate beneficiary of the 'Fortress India' strategy. The strengthening Russia-China axis makes India's self-reliance in aerospace mandatory. With an order book exceeding ₹80,000 crore and the government’s push for indigenous platforms like the Tejas Mk1A, HAL is a structural play. Unlike private players, HAL has the sovereign backing to navigate complex technology transfers that are now being denied to China by the West.

4. Reliance Industries (RELIANCE) | Sector: Energy & Retail

Reliance is a complex play. Its O2C (Oil-to-Chemicals) segment benefits from the ability to process heavy, discounted crudes (like Russian Urals), but its retail and telecom arms are exposed to domestic consumption trends. In a world of volatile energy, Reliance’s integrated model provides a buffer that standalone OMCs lack. We are watching their 'New Energy' pivot closely, as it represents the long-term hedge against the Russia-China energy axis.

5. PI Industries (PIIND) | Sector: Agrochemicals/CSM

PI Industries excels in the Custom Synthesis and Manufacturing (CSM) space. They have a 'moat' in their relationship with global innovators who are increasingly wary of intellectual property (IP) theft in China. PI’s asset-light model and strong balance sheet make it a defensive growth play in a volatile geopolitical environment.

6. Tata Elxsi (TATAELXSI) | Sector: ER&D

Tata Elxsi represents the 'Loser' or 'At-Risk' category in a specific context: Tech hardware exposure. While their software services are world-class, any disruption in the global semiconductor supply chain (often routed through China/Taiwan) can delay their ER&D projects in the automotive and broadcast sectors. Investors should monitor their margin guidance closely if trade tensions escalate to a full-blown tech blockade.

Expert Perspective: The Bull vs. Bear Debate

"The 'China Plus One' narrative is the most significant structural trend for Indian equities since the 1991 liberalization. We are seeing a total realignment of the global CAPEX cycle toward the Indian subcontinent." — Senior Strategy Analyst, WelthWest Research

The Bull Case: Bulls argue that India is in a 'sweet spot.' It is the only country that can offer the scale of China with the democratic alignment of the West. They believe the Nifty Manufacturing Index will continue to trade at a premium as earnings growth outpaces the broader market.

The Bear Case: Bears worry about 'Secondary Sanctions.' If the US decides to penalize any nation or firm that facilitates trade for the Russia-China bloc, Indian companies—especially in the banking and energy sectors—could find themselves in the crosshairs. Furthermore, they argue that high energy costs (stagflation) could kill the domestic consumption story before manufacturing fully takes off.

Actionable Investor Playbook

- The 'Core' Buy: Accumulate high-quality EMS and Defence stocks on dips. Focus on companies with a Debt-to-Equity ratio below 0.5 and a proven track record of executing large-scale PLI targets.

- The 'Energy' Hedge: Keep a portion of the portfolio in domestic gas players or renewable energy firms to offset the risk of a Brent crude spike above $100.

- The 'Sell' Trigger: Lighten positions in companies with more than 20% revenue exposure to the Chinese domestic market or those heavily reliant on Chinese raw materials without a 12-month de-risking plan.

- Time Horizon: This is a 3-5 year structural play. Do not get shaken by short-term volatility caused by diplomatic 'grandstanding.'

Risk Matrix: What Could Go Wrong?

- Global Stagflation (Probability: High): Persistent high energy prices combined with slowing global growth could dampen demand for Indian exports, despite the manufacturing shift.

- Secondary Sanctions (Probability: Medium): US Treasury actions against Indian firms dealing with sanctioned Russian entities could lead to a sudden de-rating of affected stocks.

- Currency Volatility (Probability: Medium): A strengthening Dollar (DXY) amid geopolitical flight-to-safety could pressure the Rupee, increasing the cost of imported components for manufacturers.

What to Watch Next

Investors should mark their calendars for the following catalysts:

- June 2024: Post-election policy announcements regarding the next phase of PLI schemes (PLI 2.0).

- U.S. Presidential Polls: Any shift in Trump’s 'Reciprocal Trade Act' rhetoric will directly impact Nifty IT and Manufacturing sentiment.

- OPEC+ Quarterly Meeting: Watch for any production changes that signal a response to the Russia-China energy alignment.

- RBI Monetary Policy Committee (MPC): Commentary on 'imported inflation' will be the key signal for banking and auto stocks.

Disclaimer: This content is generated by WelthWest Research Desk based on publicly available reports and is for informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Always consult a qualified financial advisor before making investment decisions.